.svg)

The Rate Tailwind Has Reversed. What It Means for Australian Real Estate Credit

The rate tailwind that supported Australian property through 2025 is gone. Every cut the RBA made last year has been unwound. This is not the next phase of the same cycle. It is a different rate environment, and it changes what survives underwriting written in the past three years. The distinction matters most in credit, where the gap between a senior first mortgage and a highly geared position is the gap between insulation and loss.

1. The cycle in full

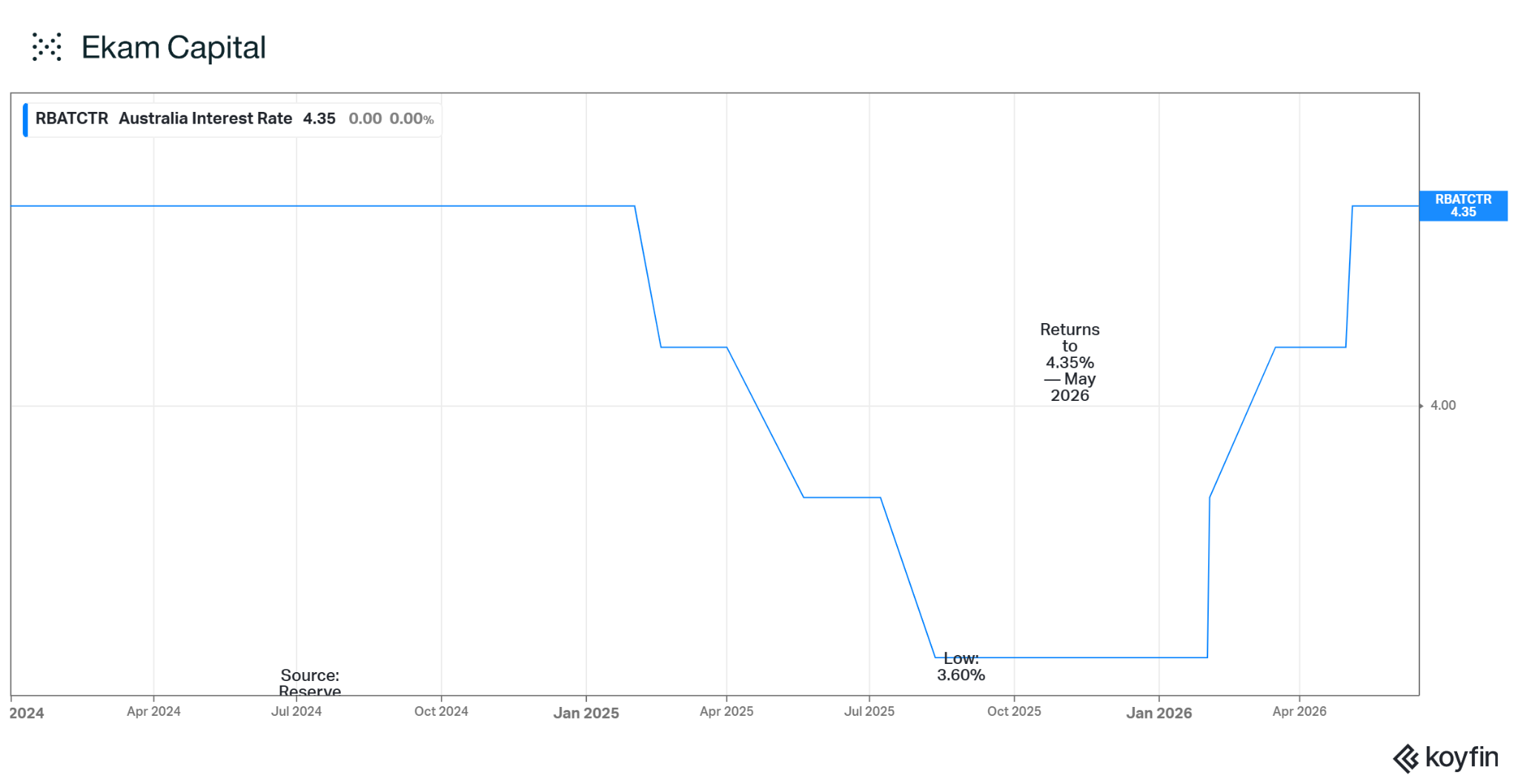

The RBA cut three times through 2025, taking the cash rate from 4.35 per cent to 3.60 per cent. Those cuts lifted borrowing capacity and sentiment and fed directly into rising prices. The Board then reversed course. Three hikes followed in 2026, in February, March and May, returning the cash rate to 4.35 per cent. Every basis point of 2025 easing has been taken back. The cash rate has risen 75 basis points since the start of the year.

The Board held in June. Governor Bullock's opening statement was explicit: “Today's decision does not rule out further tightening in monetary policy if that is what is required to bring inflation down.” That is a hold with a tightening bias retained, not a pivot.

Our base case is a hold through 2027, with the first cuts unlikely before late 2027. We hold that view with low conviction. Inflation is sticky, the Board has signalled a data-dependent posture, and the clearer risk is that Australia tracks the higher-for-longer path already evident offshore rather than the relief the market priced a year ago.

2. Why inflation is the structural driver

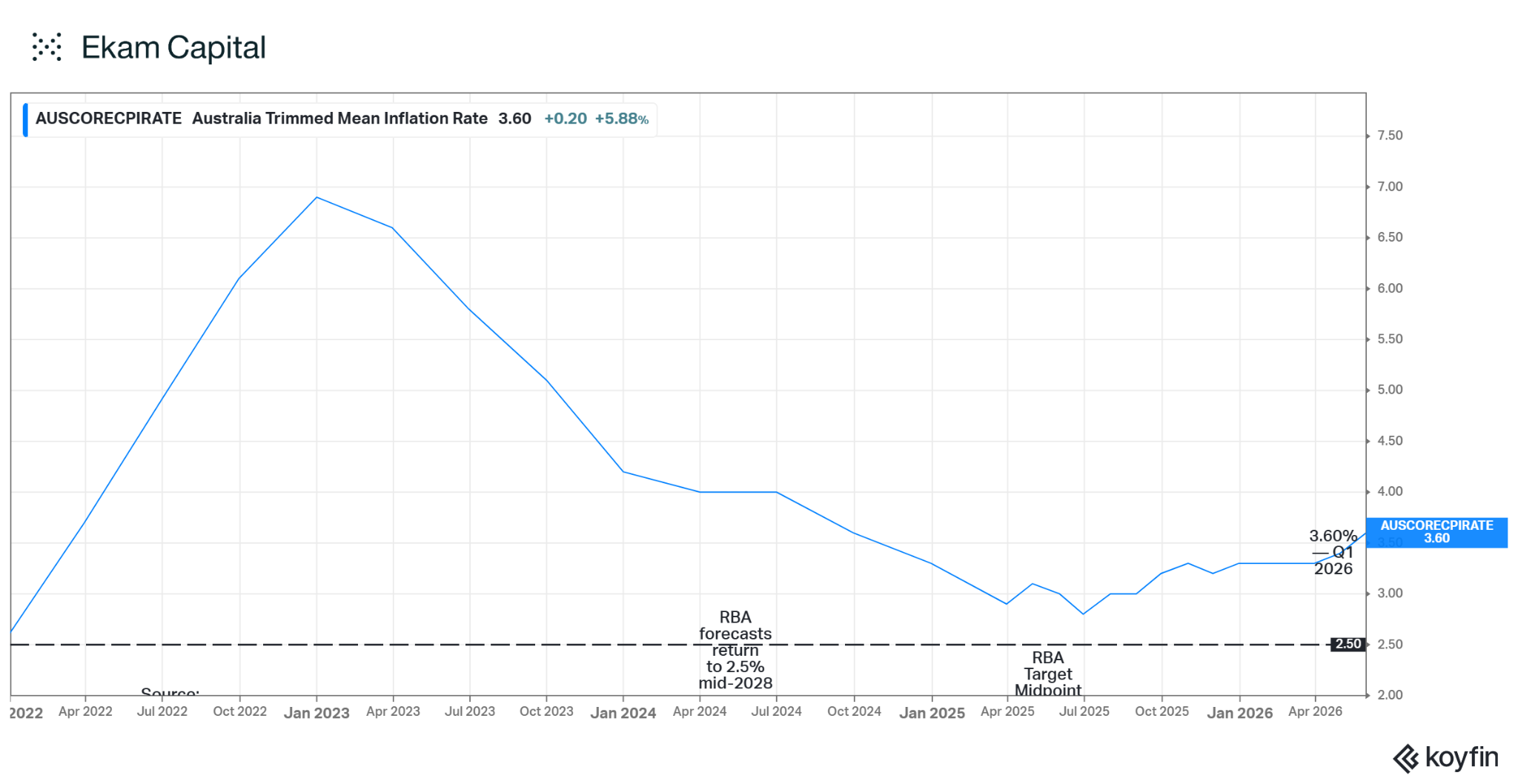

This cycle is not turning, because the core inflation problem is not solved. Trimmed mean inflation was 3.6 per cent in the year to May 2026, and the RBA does not forecast a return to the 2.5 per cent target midpoint until mid-2028. That is two years away. Trimmed mean is the measure the Board targets, and it strips volatile items like fuel. That distinction matters for what comes next.

The oil shock that drove the headline spike has largely unwound. Regular unleaded petrol rose 33 per cent between February and March when the Strait of Hormuz was closed. Brent crude has since fallen back to around US$78 a barrel by mid-June, its lowest since early March and roughly 7 per cent above its pre-conflict level, as a framework deal to end the conflict took shape. The spike is reversing at the pump.

The construction-cost question is separate, and it does not unwind symmetrically. The RBA confirmed second-round effects were passing into construction costs, including new dwellings. Those costs ratcheted up on top of capacity constraints that predate the conflict, and costs that rise on a supply shock rarely retrace at the same pace when the shock passes. Whether construction inputs follow oil down is unconfirmed. We are not assuming they do.

The market is not pricing relief either way. ASX 30-Day Interbank Cash Rate Futures implied roughly 4.48 per cent by December 2026 in mid-June. With core inflation at 3.6 per cent and the target midpoint two years out, the rate-relief thesis has no near-term basis in the data.

3. What the market data shows

The turn has already happened. Cotality’s national Home Value Index printed 0.0 per cent in May 2026, the weakest monthly result in a year. Annual growth has eased from a February peak of 10.0 per cent to 8.8 per cent. Sydney fell 0.9 per cent in May and sits 2.1 per cent below its November 2025 peak. Melbourne fell 0.8 per cent and sits 2.9 per cent below its November 2025 peak.

The leading indicators point the same way. Auction clearance rates have held below 55 per cent since late March. Capital-city sales over the three months to April were 5.4 per cent below a year earlier and 7.4 per cent below the five-year average. Advertised stock is 9.4 per cent above the five-year average in Sydney and 2.2 per cent above in Melbourne. Gross rental yields expanded to 3.59 per cent nationally in April, the first yield expansion of this cycle.

4. The trailing-data problem

The trailing data looks extraordinary, and this is where most current commentary errs. Cotality’s Pain and Gain data shows 95.9 per cent of resales made a profit last quarter, a 20-year high, at a record median gain of $365,000, on a median hold of 9.2 years. Perth dwelling values rose 91.4 per cent over the five years to May 2026.

Those numbers are real. The conditions that produced them are not in front of us. A nine-year median hold captures the entire low-rate decade, when the cash rate sat below 1 per cent for much of its duration. REA Group’s Angus Moore made the dependency explicit: if prices grew at the same rate as the past five years, buyers would pay about 61 per cent more in Sydney, 68 per cent more in Brisbane and 75 per cent more in Adelaide by 2030. That is the load-bearing assumption. It is the one the current rate environment removes.

5. What still holds

Precision is not bearishness. There are supports in this market that are rate-independent. Population growth is real and concentrated: Australia’s population grew 1.5 per cent in the year to December 2025, and Western Australia led at 2.2 per cent. Interstate and overseas migration does not slow because the cash rate is at 4.35 per cent. The structural supply shortfall persists, and it is showing up in rents. National rental growth has reaccelerated to 5.7 per cent, with vacancy at 1.7 per cent against a decade average of 2.5 per cent.

The distinction that matters is not bullish versus bearish. It is rate-dependent versus rate-independent. That distinction is the whole of the credit question.

6. Where this lands in credit

Every real estate credit exposure written in 2024 or 2025 now sits against a different rate backdrop than the one it was priced into. The transmission is specific.

Loss risk concentrates in higher-leverage positions. Where an LVR was struck against a valuation that has since softened, the equity cushion is thinner than the loan tape implies, and a backward-looking LVR flatters the real position. In a high-leverage structure that is where actual losses occur, not merely extension. Senior first-mortgage positions at reasonable LVRs are relatively well insulated, because the buffer absorbs the move.

Construction carries the extension risk. Fewer feasibilities stack at current costs and rates, and stock is taking longer to sell, which lengthens loan terms. The offset is real. Liquidity remains sufficient to absorb residual stock, and the supply-shortage thematic continues to hold, supporting the rental growth that underpins exit demand.

Serviceability and settlement are the watch items. Borrowing capacity is lower and serviceability is harder, which raises settlement risk on pre-sold stock. We are watching that closely. Holding-cost stress is the clearest pressure point, in projects that are not viable to carry at current rates.

7. The yield question

A sustained higher cash rate should lift the coupon on floating-rate credit. The base-rate move that pressures borrowers also resets lender income higher, and that is the part residential-price commentary misses.

The reality is more nuanced. Strong inflows into private credit and ample market liquidity are bidding down the pool of deals that do stack, and that pool is shrinking as feasibilities weaken. The gross-yield uplift from higher base rates is coming through below what we forecast, because competition for the good deals is compressing margin. Higher-for-longer is a tailwind for lender income in theory. In practice, deal selection now matters more than the base rate.

8. Our position

We are leaning defensive. We are stepping back from mezzanine and higher-leverage positions, where the loss mechanics above concentrate. We favour deals with a strong demonstrated ability to service, or strong fundamental drivers of demand for the underlying stock. We are cautious, deliberately.

The question for any real estate credit exposure written in the past three years is the one we are applying to our own pipeline. Was the position underwritten on rate relief, or on a senior buffer and fundamentals that survive a 4.35 per cent cash rate holding into 2027? If the answer is rate relief, the position needs re-examining. If the answer is buffer and fundamentals, the recent softness in Sydney and Melbourne is noise rather than signal. These are not the same underwrite, and this environment is separating them.

Further reading

.svg)

.svg)